The word ‘wealth’ carries with it all kinds of notions and meanings. Lots of people want to be wealthy, but that’s getting a bit ahead of ourselves.

First, let’s talk about money–specifically how much of it you have (or don’t have) and your relationship with it.

My parents ran out of money. It was 1984, and I was 12 years old. I didn’t know we were out of money–they didn’t tell us kids. All I knew was that my mother, who had always been a stay at home mom, went looking for a job. It wasn’t until recently that I found out that our home was in foreclosure, and we didn’t even have the money for basic necessities. A passage from my mother’s journal says, “our financial situation is truly at its lowest ebb so far . . . we are chained by debt and it’s terrible.” As the parents of 6 kids, the stress they felt must have been enormous [ed-My parents both died in their late 50s, so I can’t ask them more about it].

My family in early 1980s. It was the best of times, and the worst of times. I’m the little guy sporting the bowl cut and the awesome belt buckle.

After some rough times, they slowly pulled out of the crisis. My mom, who never finished college, got a job as a secretary that paid the day-to-day bills, and my dad, as serial entrepreneur, was able to put together some “deals” and earn some commissions. We didn’t lose the house, and things stabilized.

To my parents’ credit, I was not fully aware of the details of this “crisis,” but its effects were evident in our lifestyle during these lean years.

We never ate out at sit-down restaurants, and on the occasion we ever ate “Dee’s Hamburgers” (a local Salt Lake City fast food chain similar to McDonalds), we would get only the basic hamburger–never a drink or fries. Baloney was the only sandwich meat, and we only used powdered milk. My dad gave me home “bowl” style haircuts. We used long distance calls very rarely, and only for special occasions. We lived on the minimum.

At the time it felt normal and I was happy. I just knew we were very careful about what we chose to spend money on. I knew early on that if I wanted things, I would have to earn them. I had no expectations that things would be given to me. This propelled me to start a business mowing lawns around the neighborhood, and I set my goal to earn a scholarship to pay for college.

Your Relationship with Money

We all have unique stories about money. We don’t get to choose them. It’s how we grew up. It’s what we saw our parents do.

Think about your childhood. What kind of house or apartment did you live in? What kind of cars did you have, or did you have one at all? How did your parents handle money? What were birthdays like? How did your parents handle holidays and gifts? Were they modest or extravagant? Was there abundance or scarcity?

Did your family travel? If so, was it by car or plane? Did you stay in hotels? Did you camp?

Did you eat out a lot? How much food did you have around the home? Was it name brand and prepackaged or was it mostly basic ingredients? Did you use coupons?

How did you handle repairs–was it mostly do it yourself, pay a repairman, or leave things broken?

What kind of clothes did you wear? Did you have an allowance?

Did you work outside the home as a teen? Did you have to pay for things, or did your parents take care of it all? Did you or your parents pay for college? Your wedding?

How you earn, spend, and manage money today is largely due to how you experienced money growing up. My experiences still linger with me today (just ask my kids about how I complain when the lights are left on).

Childhood money experiences combined with your personality type (it’s worth knowing what it is) form your “money personality.” We each have one. It can be complex and difficult to understand. Most of us have not thought much about it, and a lot of it is subconscious.

But, like many things in life, the more you understand about “why” you do and think certain ways, the more successful you can be at fixing or building on where you are.

Three Dimensions of Money

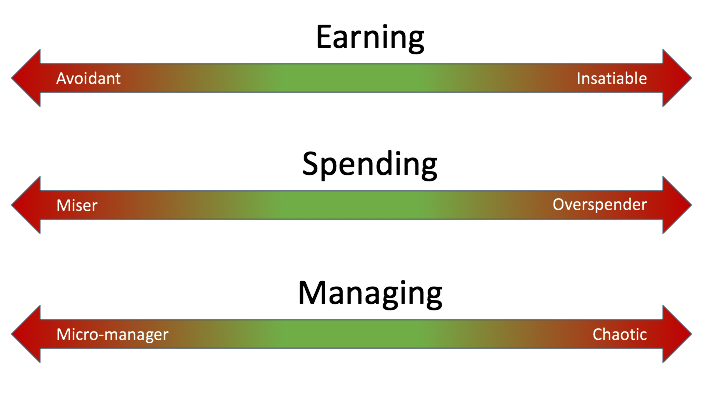

Eileen Gallo, Ph.D. writes about a “three-dimensional” relationship with money. The three dimensions are how we earn it, how we spend it, and how we manage it. On each dimension, there is a spectrum. At the extremes are the potentially unhealthy behaviors. Not surprisingly, the middle is the more stable region. Take a look at the figure below and consider where you fit on each of the dimensions. Now consider where your spouse or significant other is.

The Three Dimensions of Money

I lean toward the right on earning and toward the left on spending and managing.

Earning

This is the spectrum of how we get money. At the extreme left are people who view money as “filthy lucre.” They prefer that all society would share common goods and services. They feel no need to earn money. They are judgmental of the evils and corruption of money.

The theory of Communism may be summed up in one sentence: Abolish all private property. –Karl Marx

At the extreme right are the people who never have enough. Money is a way to keep score, and they want to win. It’s survival of the fittest, and if you can’t keep up, get out of the way. They may step on laws and people to accomplish their goals.

Greed is good. -Gordon Gekko from 1987 film Wall Street

Spending

This is the spectrum of how we save or spend money. At the extreme left are characters like Scrooge from Charles Dickens A Christmas Carol. These are extreme penny pinchers, even when they don’t have to be. They get pleasure out of holding (on to) their money, and it causes extreme pain to spend it. They don’t get out much (a behavior too highly correlated with actually spending money). They are likely to die with a large hoard of cash.

Christmas is a poor excuse every 25th of December to pick a man’s pockets. — Scrooge, A Christmas Carol by Charles Dickens

At the extreme right are people who can’t hold on to money to save their life. They spend money that they don’t have. They have numerous credit cards all maxed out, and they have likely declared personal bankruptcy. They may have YOLO as a bumper sticker.

I love money. I love everything about it. I bought some pretty good stuff. Got me a $300 pair of socks. Got a fur sink. An electric dog polisher. A gasoline powered turtleneck sweater. And, of course, I bought some dumb stuff, too. –Steve Martin

Managing

This is the spectrum of how we organize around money, including paying bills, tracking expenses, and investing. At the extreme left are the people who manage every last cent. They have tracked every purchase since they were 12 years old (they can tell you what they spent on diapers and wipes for the year 2008). They love spreadsheets and calculations. They run numbers just for fun on Friday nights. They dream in terms of the rule of 72, asset allocations, safe withdrawal rates. They calculate and recalculate at least monthly the number that will allow them to retire early (the internet has exploded with blogs of these people).

Never call an accountant a credit to her profession; a good accountant is a debit to her profession. -Charles Lyell

On the far right are the folks whose bills sit unopened under piles and piles of papers scattered around the house. They see little to no correlation with their salary and what they spend. They have never thought much further than the next paycheck. Working 9-5 for 40 hours a week is the routine. That’s just what life is, why would they question it. They live for the next TV show and the weekend. They think retirement planning is boring, so they’ll look into it when they’re around 59 or 60 (5 years should be plenty of time to figure things out).

One of the advantages of being disorderly is that one is constantly making new discoveries. –A. A. Milne

Now What?

Now that you’ve spent some time thinking about your early relationship with money and where you fit on the three dimensions of money, what’s next?

Well, hopefully, you have more insight into where your strengths and weaknesses are. If you are already on track with all your financial ducks lined up, then congratulations!

However, if you are someone who sees potential to strengthen your relationship with money in one or all of the three dimensions (earning, spending, and managing), stay tuned as we dive into some of the details in future posts.

What do you think? Have you ever thought about your money personality? Where do you fit on the three money dimensions? Share your thoughts below.

Matt Morgan, MD writes about how mastering the first habit is like pushing the power button on your life. Subscribe to his e-mail list and follow him on Twitter and Facebook.

Well done. I like the view of left and right extreme. It seems a lot of people live in or speak of the extremes. It is hard to have an intelligent conversation in the middle range.

But wait, are you saying some people don’t find it fun to run numbers on Friday night? LOL

The extremes do create more drama and discussion. Being moderate and reasonable isn’t as exciting.

I’m just slightly to the right when it comes to earning. Just slightly left when it comes to spending. And just slightly left when it comes to managing. I check my Personal Capital account a LOT! But I’m also not as obsessive about my budget either. A good majority of my friends slide way to the right when it comes to spending and managing their money. I notice that as I go more to the left, it gets harder and harder to relate to them.

Personal Capital is a great tool for consolidating all your accounts in one place. When you combine saving with compound interest, watching the graph go up can be pretty fun!

You painted a pretty accurate picture of our growing up years. Most of me is glad because we all seem to value the meaning of earning money through work. I am sad for the stress is caused our parents. But, to their credit, I too, remember being happy and having enough. I still find satisfaction in finding a “good deal”. I love the challenge of staying in a budget, but we have the luxury of not having to stress. I love having the means to bless the lives of others who do struggle. It’s such a blessing!

Thanks, Sis. No question that we learned the value of a dollar. I recall this quote in Dad’s office, “Good things come to those who wait, but only the things left by those who hustle!”